For decades, the US dollar has held the title of the world's dominant reserve currency. This status didn't come by chance: after World War II, the US emerged as the world's largest and most stable economy, and the dollar was formally established as the backbone of the global monetary system. Backed by the strength of the US economy, the depth of its financial markets, and its political stability, the dollar became the currency most central banks and global institutions turned to for safety and liquidity. As a result, the dollar has long been the anchor of global trade and finance. By the 1980s, for instance, many Gulf countries began pegging their currencies on the greenback. Yet in 2025, that dominance is showing signs of strain. In fact, the dollar just experienced its worst start to a year in over a half century-falling 10.7 percent in the first six months alone.1

This shift has left many investors asking: Why is the dollar weakening and what should I do about it?

What's Driving the Dollar's Weakness?

- Overvaluation and the Case of Normalization

One reason the dollar may be losing momentum is that it appears overvalued by historical standards. Currency valuation is influenced by many factors-interest rates, trade balances, capital flows, and economic fundamentals. On several of these fronts, the dollar has looked expensive for some time. According to the Bank for International Settlements' real effective exchange rate index, which adjusts for inflation and compares the dollar to a basket of other currencies, the dollar has consistently traded well above its long-term average.2

The overvaluation has made US goods and services more expensive abroad, contributing to persistent trade deficits and reducing the competitiveness of American exports. At the same time, it increases the burden for emerging market economies that have borrowed in US dollars, especially as global interest rates rise.

Historically, such periods of dollar strength are difficult to sustain indefinitely. Many analysts believe the greenback could be due for a multi-year weakening cycle as global growth rebalances and the appeal of non-dollar assets increases. - Tariffs and Trade Policy: A New Source of Uncertainty

A more pronounced catalyst came in the form of new US tariff announcements. These policies have injected fresh uncertainty into the global economy, eroding investor confidence in the dollar.

Historically, economic uncertainty has actually strengthened the dollar, as global investors sought out US assets as a safe haven. But this time is different. The newly proposed unilateral tariffs could compress profit margins for US companies, curb consumer confidence, and ultimately slow GDP growth. In response, investors are shifting capital abroad, weakening demand for the dollar.

Additionally, a slowing economy may lead the Federal Reserve to cut interest rates. Currently, the bond market is pricing in two to three rate reductions this year.3 Lower interest rates make the dollar less attractive relative to higher-yielding currencies, adding to its recent downward momentum. - Rising Fiscal Concerns and Debt Sustainability

Another factor weighing on the dollar's long-term outlook is the growing concern over the US fiscal position. In recent years, the federal government has run increasingly large budget deficits, with debt levels now exceeding 120 percent of GDP-compared to 102 percent ten years ago and just 61 percent two decades ago.4 While the US has long enjoyed the privilege of borrowing in its own currency at relatively low cost, investors are beginning to question how sustainable this dynamic is in a higher-rate environment.

Rising interest payments on the national debt-now one of the largest line items on the federal budget-are crowding out other government priorities and increasing the risk of fiscal instability over the long term. If markets begin to demand higher yields to compensate for this risk, the dollar could face additional downward pressure. This issue is compounded by persistent political gridlock, which makes structural deficit reduction increasingly difficult to achieve.

A Shift in Global Sentiment

While the US dollar remains dominant, its share of global currency reserves has declined-from over 70 percent in 1999 to 57 percent at the end of last year.5 As the world becomes increasingly multipolar, more countries are exploring alternatives.

Nations like China, India, Russia, and Brazil have even floated the idea of creating a new digital currency called "The Unit," though any such initiative faces serious structural and political headwinds.

At the same time, more countries are diversifying their USD holdings and seeking to reduce dependence on it for trade. There is growing interest in forming "currency blocs" that facilitate trade in local currencies-particularly among emerging economies.

This is especially relevant for countries with significant US dollar-denominated debt. During times of market stress, the dollar typically strengthens due to its safe-haven appeal, raising borrowing costs at the worst possible time.

Reducing dependence on the dollar is also a strategic goal for rising powers like China, which seeks to exert greater influence on global trade and finance.

Whatever the motivations, the de-dollarization narrative is gaining momentum.

The Dollar's Enduring Role

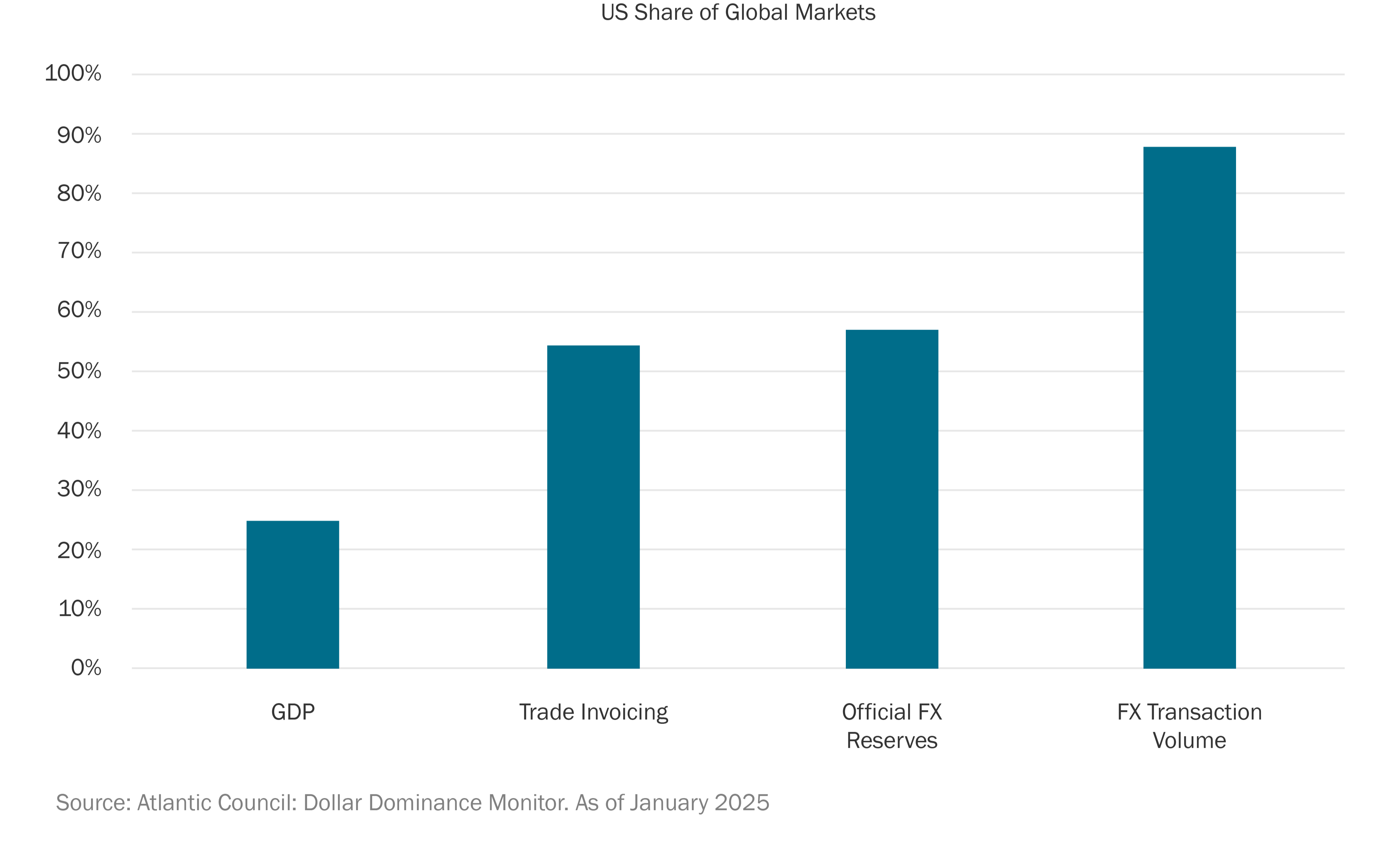

Despite the de-dollarization trend, it’s important to maintain perspective: the US dollar still holds a uniquely dominant position in global finance. While its share of official foreign exchange reserves has declined to 57 percent, the next closest competitor—the euro—accounts for just 20 percent.6

The dollar is also involved in nearly 90 percent of global foreign exchange transactions, underpins roughly half of global trade invoicing, and accounts for 42 percent of SWIFT payments.7 In comparison, the US economy represents just 25 percent of global GDP and 12 percent of world trade8, illustrating how deeply embedded the dollar is in the global system.

So while diversification efforts are real and growing, no other currency currently rivals the dollar’s liquidity, trust, or global acceptance. For now, it remains the primary medium for international commerce and financial exchange—a status that’s unlikely to change in the near term.

Still, even a gradual shift in the dollar's role can create ripple effects across global markets—and potential opportunities for investors.

How Should Investors Respond?

While the dollar’s weakness may seem like cause for concern, it also creates opportunity—particularly for internationally diversified investors.

Over the past decade, US stocks have significantly outperformed their international counterparts. The S&P 500 delivered an average annual return of 13.65 percent, compared to just 6.12 percent for the MSCI All Country World ex-USA Index.9 This disparity was accentuated by the strength of the dollar, which diluted foreign equity returns once converted back into US currency.

However, when the dollar weakens, that dynamic reverses. US investors benefit from stronger foreign currencies when translating those returns back into dollars. So far this year, international equities have outpaced US equities by over 12 percent, thanks in part to currency tailwinds.10

In anticipation of this shift, we’ve continued to emphasize global diversification across client portfolios, with increased allocations to international and emerging markets. These regions—particularly emerging markets—stand to benefit as many of their companies carry large amounts of US dollar-denominated debt. As the dollar weakens, the real burden of that debt shrinks—improving balance sheets and increasing investor appeal.

The Bottom Line

The recent slide in the US dollar is being driven by a mix of cyclical corrections, shifting trade policies, and long-term fiscal concerns. While this may raise questions about the dollar’s future role in the global financial system, it also underscores the importance of diversification.

Right now, portfolios with thoughtful allocations to both developed and emerging international markets may stand to benefit. A weakening dollar enhances the potential returns of foreign assets—reminding us that global diversification isn’t just a long-term principle; it’s a near-term opportunity.

If you haven’t recently reviewed your portfolio, now may be a prudent time to do so. As always, we’re here to help you navigate these shifts with confidence and clarity.

- FactSet: DXY Index from 1/1/2025 through 6/30/2025

- Bank for International Settlements via FRED

- CME Group: Fed Fund Futures

- FRED: Federal Debt: Total Public Debt as Percent of Gross Domestic Product

- IMF Currency Composition of Official Foreign Exchange reserves (COFER)

- IMF Currency Composition of Official Foreign Exchange reserves (COFER)

- Atlantic Council: Dollar Dominance Monitor. As of January 2025

- IMF World Economic Outlook (April 2025)

- Morningstar Direct: Total Returns from 7/1/2015- 6/30/2025

- Morningstar Direct: Total Returns from 1/1/2025 – 6/30/2025