Key Takeaways

- With year-end approaching, it’s a good time for investors to review their portfolios for tax efficiency. A tax-efficient strategy can reduce liabilities and increase gains over time, particularly for those in higher tax brackets.

- Strategies such as tax-loss harvesting, asset location, municipal bonds and contributing to tax-deferred accounts can all play a role in minimizing taxes.

- Your Financial Advisor can guide you through these strategies and identify which approaches best suit your financial goals.

As we approach the end of the year, it's an excellent time for investors to evaluate their strategies for optimizing tax efficiency. Thoughtfully considering different asset classes and the accounts that you chose to hold them in can help lower your tax bill and, ultimately, increase your investment gains over time. The higher your income tax rate, the more beneficial it may be to consider tax optimization strategies and to weigh the tax impact when adjusting your investments.

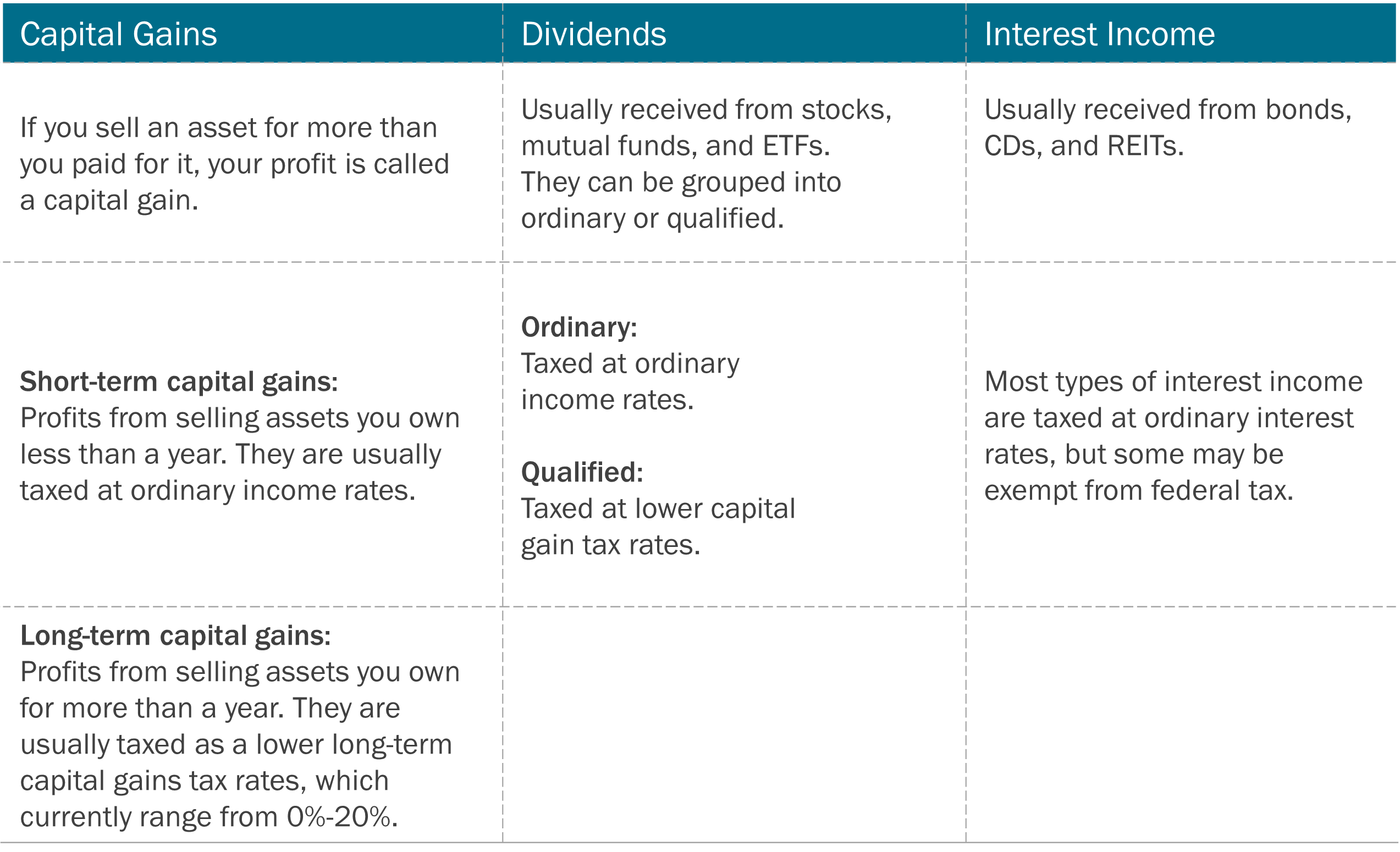

Before discussing strategies for optimizing tax efficiency, it’s helpful to understand how different types of investments are taxed. Most investment income is taxable, but your exact tax rate will vary depending on several different factors, including your tax bracket, the type of investments you hold, and how long you own them before selling them.

Lets discuss 5 different strategies that can be used to optimize tax efficiency:

1) Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that have declined in value to realize losses. These losses can offset capital gains from other investments, thereby reducing your taxable income. Additionally, if your losses exceed your gains, you can deduct up to $3,000 against your ordinary income (or $1,500 if married filing separately). Any losses exceeding $3,000 can be carried forward to future tax years, providing ongoing tax benefits.

2) Municipal Bonds

Municipal bonds, or “Munis,” are another effective strategy for enhancing tax efficiency in your investment portfolio. Munis typically offer reliable interest payments, providing a consistent income stream. The interest income earned from municipal bonds is generally exempt from federal income tax, and in some cases, state and local taxes as well. This makes them particularly attractive for investors in higher tax brackets. In addition to federally tax-exempt income, many municipal bonds carry lower risk compared to corporate bonds, making them a solid choice for many investors.

3) Exchanged-traded Funds (ETFs)

Exchange-traded funds (ETFs) can also play a significant role in a tax-efficient investment strategy for several reasons. Compared to mutual funds, ETFs generally generate fewer taxable events during the holding period, as they are often passively managed. A passively managed ETF’s objective is to track an index, which leads to low turnover. With less frequent buying and selling, ETFs can minimize capital gains distributions, helping to keep your tax bill lower. Additionally, when ETF investors sell their shares on the stock exchange to other investors, the ETF portfolio manager does not need to buy or sell any of the ETF’s underlying investments, minimizing the impact on other investors and keeping capital gains distributions low.

4) Asset Location Strategies

Not all account types are taxed the same way. IRAs and 401Ks are tax-deferred until you withdraw assets, and then taxed as ordinary income. Roth IRA contributions are made after-tax, but growth within the Roth and distributions from the Roth are tax-free, assuming certain requirements are met. Within taxable accounts (such as Trusts and Individual accounts), earnings are taxed immediately as they are paid out.

Asset location strategies involve placing investments in the most tax-efficient accounts based on their characteristics. Tax-efficient investments, such as index funds or municipal bonds, are often best held in taxable accounts because they generate lower taxable income. In addition, income from equities is generally taxed at more favorable long-term capital gains rates, so they may be better suited for taxable accounts. On the other hand, assets that tend to produce higher taxable income, like bonds or REITs, can benefit from being held in tax-deferred accounts like IRAs or 401(k)s, where income is not taxed until withdrawal. This approach helps maximize after-tax returns by allowing investments to grow more efficiently.

5) Maximizing Retirement Account Contributions

Contributing to tax-advantaged retirement accounts, like IRAs, 401(k)s and Roth IRAs, offers significant benefits. With traditional IRAs and 401(k)s, contributions are made pre-tax, reducing your taxable income in the year of contribution and allowing investments to grow tax-deferred until retirement. In addition, employer-sponsored plans like 401(k)s often include matching contributions, effectively providing "free" money to enhance retirement savings.

Roth IRAs, on the other hand, use after-tax contributions, but withdrawals in retirement are tax-free, including earnings, if certain conditions are met. Contributing to retirement accounts allows investments to grow without the drag of annual taxes, maximizing savings potential over time.

Final Thoughts

With year-end approaching, now is the time to evaluate your investment strategy and explore various tax-efficient options. SageView offers all of the strategies discussed and implements them with clients where appropriate.

We are committed to helping you navigate these strategies to maximize your financial well-being. If you have any questions or wish to delve deeper into tax strategies for your investments, please reach out to your financial advisor. Together, we can ensure that your portfolio is well-positioned for both growth and tax efficiency as we close out the year.